India’s New Income Tax Act Is Live. A Commerce Expert Explains What Actually Changed.

By Anna Leela Commerce Expert | April 2026

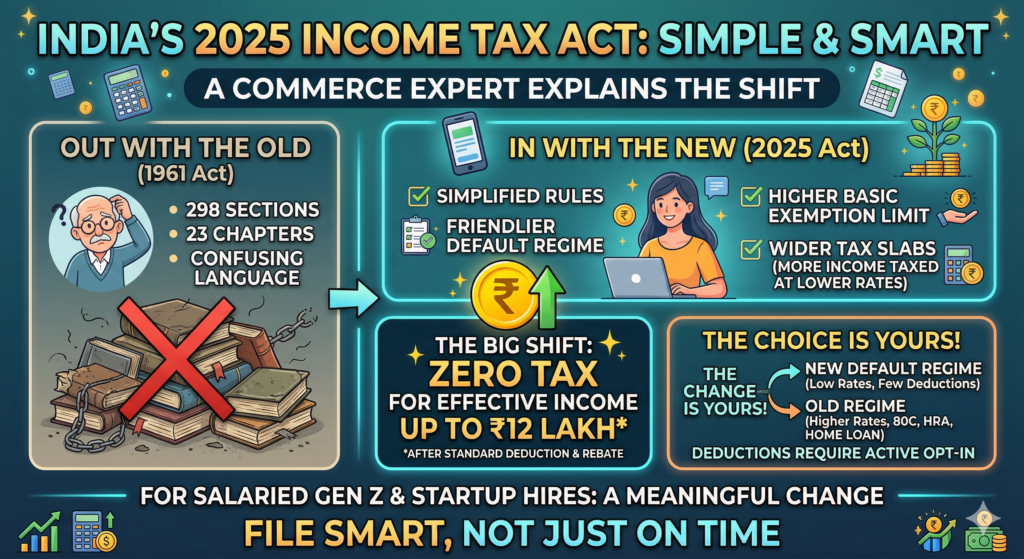

The Income Tax Act of 1961 was written before most young taxpayers were born. Drafted in a pre-liberalization India, it carried the weight of six decades of amendments, exemptions, clauses, sub-clauses, provisos, and explanations that grew year after year like barnacles on a ship. By the time it reached its final form, it had 298 sections, 23 chapters, and language so dense that even seasoned Chartered Accountants had to pause and re-read. For the average salaried millennial or Gen Z employee filing their first ITR, it was essentially a foreign language.

The new Income Tax Act, 2025 is the government’s attempt to fix that. But here’s the thing about simplification: it doesn’t automatically mean lower taxes, fewer obligations, or less paperwork. What it means is that the rules are written more plainly, structured more logically, and — in some areas — more favorably for certain categories of taxpayers. Whether it’s good news for you specifically depends entirely on where you fall in the income spectrum and what deductions you’ve been claiming.

Let’s break it down properly.

Why the Old Act Needed to Go

To understand what changed, you have to understand just how broken the old system had become.

The Income Tax Act of 1961 wasn’t born complex — it was made complex over time. Every budget season brought new provisions. Some were added to promote investment (think: Section 80C for ELSS mutual funds and PPF). Some were introduced to plug loopholes. Some existed to protect legacy arrangements — like the grandfather clauses for old insurance policies or property transactions. Each new provision had to be layered on top of existing ones without disturbing what came before.

The result was a document that referenced itself constantly. You’d read Section 10 to understand an exemption, only to find it pointed you to Section 80, which itself referenced Schedule II, which cross-referenced a notification issued under Rule 8D. For a system that touches nearly every working adult in the country, it was remarkably inaccessible.

The 2025 Act doesn’t just clean up the language — it reorganizes the entire architecture of tax law. Sections are renumbered. Chapters are regrouped by theme. The provisos and explanations that used to live as dense paragraphs appended to sections are now pulled out into cleaner sub-sections or standalone clauses. The goal, explicitly stated by the government, was to write a law that a reasonably educated taxpayer could read and understand without needing a professional to translate it.

Whether they’ve fully achieved that goal is debatable. But directionally, the intent is clear and the improvement is real.

The New Default: The Simplified Regime Is Now the Standard

One of the most consequential shifts in the 2025 Act is a structural one: the new tax regime is now the default.

Under the old framework — and until recently — the old regime with its labyrinthine set of deductions was what most taxpayers fell into unless they actively chose otherwise. The new (simplified) regime, introduced in 2020 and revised in 2023, offered lower slab rates but stripped out most deductions. It was an opt-in for people who wanted simpler math and lower rates, but didn’t necessarily serve everyone well — especially those with significant home loan interest, HRA claims, or life insurance premiums.

Now, the 2025 Act flips that logic. The simplified regime is the default. If you want the old deductions — your 80C for ELSS, your HRA exemption, your home loan principal and interest deduction — you have to actively opt in to the old regime. You have to make a deliberate choice and you have to justify it.

This matters enormously in practice. Millions of taxpayers who previously benefited from deductions without really thinking about it will now need to calculate whether opting back into the old regime is actually worth it. For most salaried employees under ₹15–18 lakh with modest deduction claims, it probably won’t be. For someone with a large home loan in a metro city, paying significant HRA, and maxing out 80C, the math might still favor the old regime.

But the burden of thinking about it, calculating it, and making that active choice now rests entirely on you.

The Slab Restructuring: What the Numbers Actually Say

The new regime’s slabs have been revised in a way that genuinely favors middle-income earners. Here’s the structure as it stands under the 2025 Act:

- Up to ₹4 lakh: Nil

- ₹4 lakh to ₹8 lakh: 5%

- ₹8 lakh to ₹12 lakh: 10%

- ₹12 lakh to ₹16 lakh: 15%

- ₹16 lakh to ₹20 lakh: 20%

- ₹20 lakh to ₹24 lakh: 25%

- Above ₹24 lakh: 30%

Compare this to the old new regime slabs from a couple of years ago, and you’ll notice the bands are wider and the rates at the lower end are gentler. The government has clearly tried to protect the ₹8–12 lakh segment — the salaried middle class that drives consumption and votes in large numbers.

But the headline number everyone is talking about is this: effective zero tax up to ₹12 lakh.

Here’s how that math works. The standard deduction for salaried individuals is ₹75,000. So your taxable income after that deduction is ₹12 lakh minus ₹75,000, which is ₹11.25 lakh. On that, you’d compute your tax according to the slabs above. That comes to approximately ₹60,000. And then — critically — you apply Section 87A, the tax rebate, which under the new Act is ₹60,000 for incomes up to ₹12 lakh. The rebate wipes out the tax entirely.

So if your gross salary is exactly ₹12 lakh, your net tax outgo is zero. Not because you’re below the basic exemption limit, but because the rebate mechanism offsets the computed tax completely.

The catch? This only works if your income is at or below ₹12 lakh. If you earn ₹12.1 lakh, the rebate drops away and you pay tax on the full slab computation — which creates a noticeable marginal tax cliff right at that threshold. This is a known structural awkwardness in the design and worth being aware of if you’re close to that band.

What Happens to the Old Deductions?

They still exist. Let’s be clear about that. Section 80C, 80D, HRA, LTA, home loan interest under Section 24(b) — none of these have been abolished. They’ve simply been moved to the opt-in old regime.

If you choose to stay in the new default regime (which, again, is now the starting point for everyone), you give up these deductions. In exchange, you get the lower, cleaner slab rates and the simplicity of not having to gather investment proofs and rent receipts and bank certificates every year.

If you opt into the old regime, you get access to all those deductions, but you pay tax at the older, slightly higher slab rates. The question then becomes pure arithmetic: do your deductions reduce your tax liability under the old regime more than the new regime’s lower rates reduce it on their own?

For someone earning ₹10 lakh with ₹1.5 lakh in 80C investments and significant HRA, the old regime might still win. For someone earning ₹10 lakh with minimal investments and no HRA claim, the new regime is almost certainly better.

The only way to know is to run both calculations — or use a tax planning tool — before the financial year ends and before your employer locks in your tax declaration for the year.

For Salaried Gen Z and Early-Career Professionals: The Practical Takeaway

If you’re in your first or second job, earning somewhere between ₹6 lakh and ₹15 lakh, here’s what you actually need to know and do.

If you earn up to ₹12 lakh: You’re likely paying zero income tax under the new default regime. Make sure your HR has your salary structure correct, your PAN is linked to your Aadhaar, and you file your ITR on time even if your liability is nil. Filing isn’t optional just because you owe nothing — and a clean filing record matters when you apply for loans or visas.

If you earn between ₹12 lakh and ₹18 lakh: This is the zone where running both regime calculations is most important. Whether you have a home loan, claim significant HRA, or contribute to NPS through your employer can genuinely shift which regime is better. Don’t assume — calculate.

If you’re a startup employee with ESOPs: The 2025 Act has clearer language around ESOP taxation timelines, which matters if your company is not publicly listed. The point of taxation, the method of valuation, and the treatment of perquisites have been restated more clearly. Worth a one-time conversation with a CA if you have significant ESOP holdings.

If you’re freelancing or have side income: The new Act addresses presumptive taxation schemes with updated thresholds. If your freelance income crosses ₹75 lakh, you may no longer be eligible for the simplified 44ADA presumptive scheme. Keep track of your total receipts across the year.

What the Simplification Actually Means Beyond Slabs

The 2025 Act’s simplification goes beyond just tax slabs and regimes. A few structural changes are worth noting even if they don’t change your immediate tax liability.

Plain language drafting. Provisions that used to read like legal riddles have been rewritten in active voice with shorter sentences. This doesn’t change what you owe, but it changes how accessible the law is to a non-expert. If you’ve ever tried to read a tax notice and felt lost, the 2025 Act’s language reform is a small but meaningful improvement.

Consolidation of dispute resolution. The Faceless Assessment Scheme and Faceless Appeals, introduced in earlier years, are now codified more clearly into the Act’s structure. This matters if you ever face a scrutiny notice or want to appeal an assessment order.

Clearer TDS provisions. Tax Deducted at Source rules, which affect everything from bank FD interest to freelance payments to rent, have been restated with more precise thresholds and timelines. If you’ve ever been confused about why your bank deducted TDS when you thought you were below the limit, the new Act’s TDS chapter is notably cleaner.

Rationalization of capital gains. The treatment of long-term and short-term capital gains — particularly from equity mutual funds and listed shares — has been restructured. The grandfathering provisions for pre-2018 gains are now stated more plainly, which matters if you’re sitting on old equity investments.

What Didn’t Change (That People Thought Might)

There was significant speculation before the 2025 Act was finalized about more radical reforms. Wealth tax was discussed. Agricultural income taxation came up in policy circles. The inheritance tax question, while not a formal proposal, generated media noise.

None of these made it into the final Act.

Agricultural income remains exempt. There’s no wealth tax. No inheritance or estate duty. The basic architecture of direct taxation — income from salary, house property, business, capital gains, and other sources — remains the same five heads of income it’s been since 1961. What changed is the expression and the mechanics, not the fundamental structure.

This is actually worth noting for anyone who consumed anxious financial content in the run-up to the Act’s passage. The reform is evolutionary, not revolutionary.

The Bottom Line

India’s new Income Tax Act is a meaningful improvement in accessibility and in the fairness of lower-bracket taxation. The zero-tax threshold at ₹12 lakh is real and significant for a large portion of the formal salaried workforce. The cleaner language and reorganized structure make the law more navigable, even if it doesn’t eliminate the need for professional advice in complex situations.

But simplification is not the same as automation, and clarity is not the same as certainty. You still need to actively evaluate which regime works better for your specific income and deduction profile. You still need to file on time. You still need to keep your financial documents in order.

The government has done its part by rewriting the law in a more human-readable form. The rest — understanding it, planning around it, and filing accurately — is still on you.

File smart. Not just on time.