India Replaced Its 60-Year-Old Income Tax Act — And Every Commerce Student Must Know What Changed on April 1, 2026

By a Professor, Anna Leela College of Commerce

Let me start with something simple. When I was a student, the Income Tax Act of 1961 was handed to us in class like a sacred text. It was thick, it was dense, and the running joke was that even the professors who taught it didn’t fully understand half of it. We memorised sections, we crammed assessment year definitions, and we hoped for the best in exams. That was the 1960s framework meeting us, students of the 21st century, somewhere in the middle.

On April 1, 2026, that era officially ended.

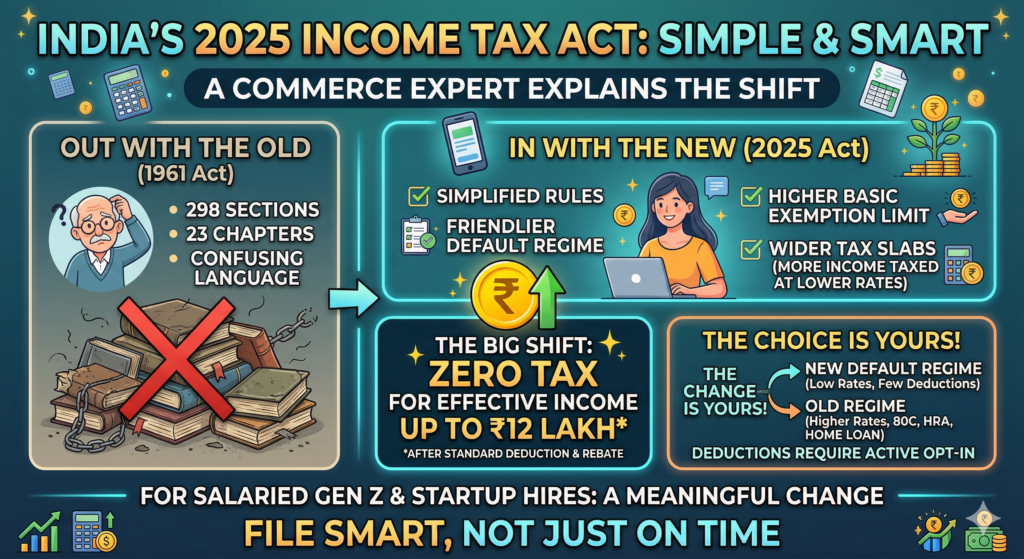

The Income Tax Act 2025 replaced the six-decade-old Income Tax Act of 1961, coming into force from April 1, 2026. It reorganises the country’s income tax provisions into 536 sections spread across 23 chapters, with the stated goal of making tax law simpler, clearer, and less painful to navigate for taxpayers, businesses, and tax professionals alike.

Now, before you dismiss this as just another government update that doesn’t affect your daily life, let me stop you right there. This is not a minor tweak. This is a structural overhaul that changes how the entire framework of direct taxation is written, read, and applied in India. And if you are a commerce student — whether you are in your second year of BCom, preparing for the CA foundation, or already clearing your Inter exams — this is the single biggest development in your subject area in your lifetime.

Let me walk you through what actually changed, why it matters, and what it means for your career.

First, a little bit of history. Why did the 1961 Act need to go?

The Income Tax Act of 1961 was amended almost 65 times through Finance Acts and numerous Taxation Laws Amendment Bills. These frequent updates — more than 4,000 individual changes — expanded the legislation considerably, leaving taxpayers navigating a vast and scattered collection of provisions.

Think about that for a moment. Over four thousand individual changes to a single law. Provisions added in 1967 sitting awkwardly next to provisions added in 2019. Language written for a pre-liberalisation, pre-internet, largely agrarian economy being applied to digital businesses, startup equity, international transactions, and cryptocurrency. The law had become a maze that even seasoned CAs and judges frequently disagreed on. That is not a tax system — that is a legal puzzle nobody fully solves.

The ITA 1961 had, over its 65 years of life, accumulated over 800 sections, hundreds of amendments, thousands of provisos, explanations, and clauses, and had become notoriously difficult to navigate. This complexity was not a feature. It was a bug that had been piling up for six decades.

The result was predictable. Litigation exploded. Cases piled up in tribunals. Businesses spent enormous resources just interpreting what the law meant, not even complying with it. Something had to give.

So what exactly is the Income Tax Act 2025?

The simplest way I can explain it to you is this: the new Act is not a new tax law so much as a rebuilt one. Same charge to tax, same rates, same deductions. What changed is everything around it — the structure, the language, the cross-references, and the sheer navigability of the statute.

They took the same house, knocked down the confusing internal walls, rebuilt the rooms logically, put proper signage everywhere, and handed it back to you. The rent hasn’t changed. The address hasn’t changed. But now you can actually find the bathroom without getting lost.

The total number of sections came down from over 800 in the 1961 Act to 536. Digital-first, faceless assessment procedures have been incorporated to reduce human interface and curb corruption. All TDS provisions, which were previously scattered across different sections, have been consolidated under a single section — Section 393. Deductions that were buried in different parts of the old Act are now regrouped logically so you don’t have to hunt through multiple chapters to understand what you can claim.

The “Tax Year” concept — and why it actually matters

Here is one of the changes that I am genuinely excited to explain in class from next semester onwards, because the old system used to confuse students every single year without fail.

Under the 1961 Act, we had two separate time period concepts — the “Previous Year” and the “Assessment Year.” Your income was earned in the Previous Year, but it was taxed in the Assessment Year. So income earned in FY 2024-25 was assessed in AY 2025-26. This dual-year reference system caused endless confusion. Students would mix up the years. Taxpayers would file under the wrong year. Even courts sometimes had to clarify which year applied to which proceeding.

The Income Tax Act 2025 replaces this by introducing a single, unified concept called the “Tax Year.” The term “previous year” has been dropped, and “assessment year” has been discontinued. The charge of income tax is now on the total income of the “tax year” of a person. Simply put, the Tax Year concept under the new Act corresponds to the Previous Year concept under the 1961 Act — but it eliminates the confusion caused by dual-year references.

From now on, income earned in Tax Year 2026-27 is reported and assessed for that same Tax Year 2026-27. No more separate “previous year” and “assessment year” to keep track of. One year, one name, one reference.

For students appearing in exams and for professionals filing returns — this is clarity that was long overdue.

The ₹12 lakh threshold — and what stays the same

I know many of you have seen this number floating around and wondered if this is a new benefit under the new Act. Here is the precise answer: the Finance Act 2025 slabs continue to apply as they are, for both old and new regimes. This means no tax up to ₹12 lakh under the new regime, or ₹12.75 lakh if you are a salaried individual.

The ₹12 lakh annual basic exemption limit has been retained with revised tax slabs to benefit middle-income groups, and the new tax regime remains the default regime. The old tax regime with its various deductions and exemptions remains available as an option for those who benefit from it.

This is important context: the 2025 Act did not create new tax burdens or remove existing benefits. It preserved what was already there and presented it in a form that is far easier to understand and apply.

The transition — what students and professionals must understand right now

Here is where it gets a little technical, but it is worth knowing because exam questions will definitely test this.

Starting April 1, 2026, the e-filing portal now supports both Acts simultaneously. In July 2026, taxpayers will file their return for AY 2026-27 — for income earned up to March 31, 2026 — using the old ITR forms and the old Act. During the same period, taxpayers will also pay Advance Tax for Tax Year 2026-27 under the new Act.

What this means is that we are in a dual-track period. The 1961 Act is officially repealed, but it continues to govern income earned before April 1, 2026. The 2025 Act governs income from April 1, 2026 onwards. The CBDT transition FAQ confirms there is “no missing year and no overlap” — income of the period before April 1, 2026 remains under the old law, and income from April 1, 2026 onwards falls under the new Act.

Additionally, the Income Tax Rules, 2026 have been notified alongside the new Act, replacing the Income Tax Rules, 1962, with ITR forms, TDS certificate formats, and audit report formats all revised to align with the new section numbers of the 2025 Act.

For practicing CAs and tax professionals, all pending appeals before CIT(A), ITAT, High Court, and Supreme Court relating to AY 2024-25 and earlier will continue to be governed by the 1961 Act. Section numbers from the 2025 Act must not be cited in briefs relating to past assessment years.

If this feels like a lot to keep track of — you are right. But that is precisely why professionals who understand both frameworks are going to be in extremely high demand over the next several years.

What this means for your career — and why I am telling you this now

I want to be direct with you here, because I think sometimes professors sugarcoat things and students only realize the significance of a change five years too late.

India just rewrote its foundational direct tax law for the first time in 65 years. Think about what that means for the ecosystem around it. Every textbook needs updating. Every coaching module needs rebuilding. Every tax software system needs to remap its section references. Every CA firm needs to retrain its staff. Every corporate finance team needs to understand the new compliance framework. Every bank, every insurance company, every NBFC that operates in the tax planning space needs people who understand what changed and what stayed the same.

This is not a small ripple. This is a large wave, and it is moving toward every corner of commerce and finance in India.

If you are a BCom or MCom student, this is the moment to go beyond your textbook. Read the actual Act. Use the section mapping tool on the Income Tax India portal, which allows you to see exactly how each old section maps to the new one. Understand the Tax Year concept well enough that you can explain it to someone who has never heard of it. That ability to explain complex things simply is worth more in the job market than you might think.

If you are preparing for the CA exams, know that the Institute of Chartered Accountants of India will align its curriculum with the new Act, and your advantage will come from understanding the logic of the restructuring — not just memorising new section numbers. The logic does not change. The principles of income taxation, the five heads of income, the rules of deduction and exemption — all of that is the same. What you are learning is still valid. You just need to know the new address of each rule.

If you are already working in finance or are a practitioner — this is your moment to upskill ahead of your peers. The dual-track compliance period is going to create genuine demand for professionals who can navigate both regimes confidently. Section mapping literacy, familiarity with the new Income Tax Rules 2026, and an understanding of how the transition framework works are immediate, practical skills with real market value.

One last thought

When the 1961 Act was drafted, India had a population of around 450 million people. There was no internet. There were no mutual funds as we know them today. There were no startups, no ESOPs, no digital wallets, no crypto. The economy it was designed for no longer exists.

The Income Tax Act 2025 does not solve all of our tax problems overnight. There will be teething issues. There will be portal glitches. There will be confusion during the transition. That is inevitable with any change of this scale. But the direction is right, and the intention — to make taxation more readable, more navigable, more honest in its language — is something that every commerce student should appreciate.

You are the first generation of tax professionals who will learn taxation under this new framework from the ground up. That is not a burden. That is an advantage. You will not carry the muscle memory of the old system, which means you can internalize the new one more cleanly and more deeply than anyone who has spent 20 years navigating the old maze.

Pay attention to this. Study it seriously. It is not just going to appear in your exams — it is going to define your professional environment for the next several decades.

And with that, I will see you in class.